Introduction

Applying for a loan can feel overwhelming, especially when you’re unsure how lenders assess your loan application. But understanding the process can make all the difference. When you know what lenders are looking for, you can present a stronger application and maximize your chances of approval.

This guide will explain how banks evaluate your loan application and how lenders evaluate loan applications and provide expert tips to help you succeed. From key trends to common myths, you’ll walk away with everything you need to know to approach your loan application confidently.

Lenders are organizations like banks, NBFCs, or fintech companies that give you loans or credit.

Expert’s View on Loan Evaluations

Key Trends and Updates

The lending industry has seen many changes in recent years. With the rise of online loan applications, lenders are using advanced digital processes to assess your eligibility. Here are some key trends experts want you to notice in how banks evaluate your loan application.

Digital Loan Applications

Many lenders provide user-friendly platforms to track your loan application status, ensuring faster processing and greater transparency throughout the approval process.

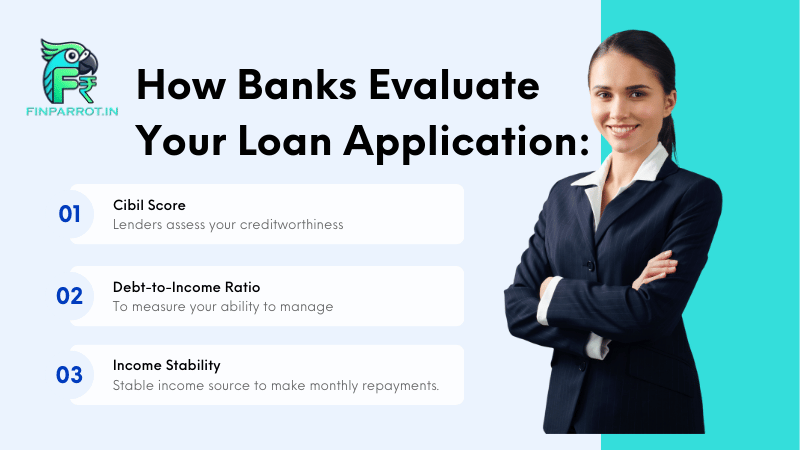

Credit Score Focus

Your credit score has become one of the most crucial/important evaluation factors. Scores above 750 generally indicate creditworthiness.

Paperless Documentation

Thanks to digital systems, there’s less paperwork today. Many lenders only ask for scanned copies of essential documents through their portals for your loan application form.

Employment or Income Stability

Lenders evaluate your income consistency and job security to ensure you can repay the loan on time. Stable employment history matters for salaried individuals, while consistent business income is key for self-employed individuals.

Debt-to-Income Ratio

Considering how much of your monthly income goes toward paying debts. A lower DTI (under 40%) is better. It indicates better financial management, making you more likely to qualify for a loan.

Why this Topic is Important Now?

If you’re applying for a personal loan, home loan, or business loan, it’s very important to know how banks evaluate your loan application. Here’s why:

- Saves Time: When you know what documents and requirements are needed in advance, you can get everything ready. This means fewer delays and a lower chance of rejection!

- Improves Approval Odds: A well-prepared loan application that is accurate and detailed significantly increases your chances of getting the loan you need.

- Secures Better Terms: A solid financial profile is like a good credit score, and a stable income can help you score lower interest rates and have more flexible repayment options!

Insights from Industry Professionals

Insight 1: Build a Strong Credit Score

A high credit score is the best thing to get loan approvals quickly. Here’s what the experts suggest you do to maintain or improve it:

- Always pay your EMIs and credit card bills on time.

- Avoid making frequent loan inquiries, as it can negatively impact your score.

- Regularly check your credit report to identify any wrong updates and report inconsistency to the credit bureau for regression.

- Don’t have much credit history? Consider getting a small credit card, using it responsibly, and paying bills on time to build your score gradually.

Insight 2: Keep Your Debt-to-Income Ratio in Check

- Lenders assess how much of your monthly income goes toward existing debt payments. Experts recommend keeping your debt-to-income ratio below 40%. This shows lenders that you can handle additional loan duty, commitment, or responsibility without stress.

Insight 3: Provide Complete and Accurate Information

- Whether you’re filling out a Lender loan application status check or submitting documents for the loan application, incomplete or inaccurate information is the most common reason for rejections.

To avoid this:

- Double-check your documents before uploading them to an online loan application.

- Ensure you submit your accurate proof of income, employment, and identity.

- Be transparent about your liabilities—lenders will verify everything anyway.

Read also – RBI New Loan Rules 2025

Why Trust These Experts?

Expert Credentials and Experience

Trusted Expert Advice: These tips come from financial professionals who have years of experience reviewing applications and spotting common mistakes.

Accurate Results Backing the Advice

Countless loan seekers have benefited from these tips, securing funding even after being denied elsewhere. For example, following a few tweaks to their credit profile, applicants drastically improved their personal loan application approval rates.

3 Common Myths about Loan Applications

Myth 1: A Single Rejection Prevents Future Approvals

A rejection doesn’t close the door to future loans; improving your profile can help with future applications.

Myth 2: Only People with Standard Incomes Can Get Loans with Low Interest

Self-employed individuals can also get loans with competitive rates if they have a strong financial profile.

Myth 3: You Can’t Get a Loan with a Low CIBIL Score

While a low CIBIL score can make it harder, there are still options like secured loans or loans with higher interest rates for those with lower scores.

FAQ

How do banks verify loan documents?

Banks verify loan documents by cross-checking them with government databases, contacting employers, and verifying addresses and financial statements.

How do banks decide who gets a loan?

Banks decide who gets a loan based on the applicant's creditworthiness, financial stability, income level, and ability to repay the loan on time.

Conclusion

Understanding how lenders evaluate loan applications helps you navigate the lending process more efficiently and increases your chances of approval. By addressing the common myths, you can confidently approach your loan application, knowing that factors like a strong credit score, a low debt-to-income ratio, and complete documentation will boost your chances of success.

Whether you’re applying for a personal, business, or home loan, ensure your financial profile reflects your ability to repay the loan. With expert tips and an informed approach, you’ll improve your chances of securing the loan you need with favorable terms.

Most Related Topics

Bank Loans, NBFC Loans, and Fintech Loans